2019 has been a banner year for stocks, capping an incredible decade. The S&P 500 has risen 371% from its low in March 2009.

The performance is even more impressive when compared with global market averages. Over the same time frame, the MSCI World Index is up 237%, while the Vanguard FTSE Emerging Markets ETF has risen 110%.

That’s right. Despite all the concerns about our “fading” superpower status, American stocks dramatically outperformed the rest of the world in the past decade.

And they did it during a period covering both Republican and Democratic administrations amid intense political partisanship.

I believe the red, white and blue bull market has more room to run. But I also think it’s time to add more global stocks to your portfolio.

Here are three reasons why…

- You are probably “underweight” in global stocks. The average U.S. investor has roughly 85% of their portfolio in U.S. assets, according to Vanguard.But the U.S. makes up “only” about 55% of global market cap, based on MSCI’s All Country World Index.That means the average American investor is “overweight” in U.S. stocks by 30 basis points. This is partially the result of what academics call “home-country bias.”

Put another way, people tend to own what is familiar. So U.S. investors buy American stocks, Japanese investors buy Japanese stocks, German investors buy German stocks and so on.

There’s nothing wrong with this. Peter Lynch said to “invest in what you know,” and he did pretty well…

But we live in a global economy, and your address should not limit your investing.

I’m not saying you should dump all your U.S. stocks and buy all foreign ones. I’m talking about rebalancing your portfolio after a heady decade for U.S. stocks.

After all, there’s nothing wrong with trimming profits here and buying something over there that hasn’t had the same kind of gains in recent years…

Especially when these gains have other implications as well. Fidelity says 57% of baby boomers are holding more equities than the firm recommends. That’s largely due to the bull market of the last 10 years.

I’m taking what Peter Lynch’s old firm says about stocks a step further: Most Americans need to rebalance the stocks themselves and find more room for international equities.

- We’ll see a reversion to the mean. A decade of American outperformance has pushed U.S. valuations (compared with those of global stocks) to extreme levels.The S&P 500 trades at a forward price-to-earnings ratio of 17.8, compared with 12 to 13 for European and emerging market stocks, according to Yardeni Research.Because of the size of our economy, strength of our capital markets and relative stability, U.S. stocks historically trade at a premium to global competitors.

But that premium is now larger than normal, and it’s at its widest since 2001.

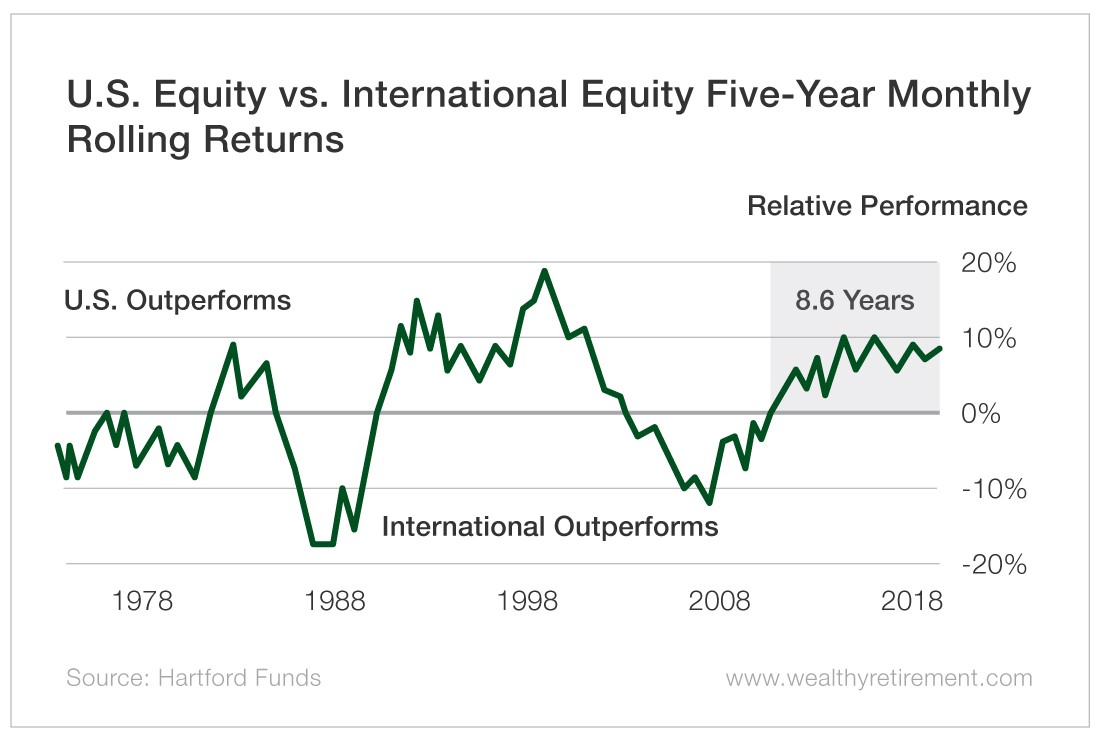

These things tend to run in cycles. “Since 1970, the outperformance cycle of U.S. versus international stocks has lasted an average of 7.5 years,” according to Hartford Funds.

“We’re currently [nearly nine] years into the current cycle of U.S. outperformance, which suggests the tides may be getting ready to turn.”

- It’s the earnings, stupid. The best reason to own international stocks: That’s where the earnings growth is coming from. This is particularly true of emerging markets.Emerging markets represent only 12% of global market cap, as covered by the MSCI ACWI Investable Market Index (IMI).But emerging markets account for 42% of global corporate revenues, up from less than 10% in 2003.

During that time frame – 16 years – emerging markets have outperformed U.S. stocks despite their volatile nature and America’s tremendous run in the past decade.

To that point: Because they are volatile and prone to political upheaval, emerging markets are not a great trade.

But they are a great long-term investment. The growing middle classes of China and India (most notably) want the same type of consumer goods Americans have long taken for granted.

Twenty years ago, this meant going from a bike to a motorcycle to a car. Ten years ago, it meant increased ownership of TVs, washing machines and other modern conveniences. Today, it increasingly means luxury goods and financial services once common only in the West.

Foreign Stocks Boost Returns

Finally, emerging markets are a great hedge against weakness in the U.S. dollar. As with America itself, the dollar has done remarkably well despite widespread forecasts of its demise.

I don’t believe the dollar is set to become toilet paper, as many doomsayers predict. But the federal deficit is now back over $1 trillion, and it’s hard to imagine the greenback won’t at least soften in the coming decade.

If and when that occurs, international markets – emerging and developed – will perform better as their currencies rise in relation to the dollar.

[adzerk-get-ad zone="245143" size="4"]About Aaron Task

Aaron is an expert writer and researcher who formerly served as editor-in-chief at Yahoo Finance, digital editor of Fortune, and executive editor and San Francisco bureau chief of TheStreet. You may have also seen him as a guest on CNBC, CBS This Morning, Fox Business, ABC News and other outlets.

A prolific writer and commentator, Aaron is the former host of Yahoo Finance’s video program The Daily Ticker. He has also hosted podcasts for Fortune (Fortune Unfiltered) and TheStreet (The Real Story). His latest on-air passion project, Seeking Alpha’s highly rated Alpha Trader podcast, features top Wall Street experts dissecting the market’s latest news and previewing significant upcoming events. He also regularly provides analysis for the free e-letter Wealthy Retirement, which we will be republishing here on Investment U.