In the summer of 2018, I analyzed the safety of master limited partnership (MLP) Energy Transfer Partners. At the time, the stock received a “C” rating.

The issues were that cash available for distribution (CAD), a measure of cash flow for MLPs, was heading lower and the company’s debt was too high.

Four months later, the MLP merged with its parent company, Energy Transfer Equity, and renamed itself Energy Transfer LP (NYSE: ET).

Let’s take a look at the new combined company and see if the distribution (partnerships pay distributions instead of dividends) is any safer.

CAD is soaring. This chart says it all.

This year, CAD is forecast to grow 13%.

That helps keep the payout ratio to a low 43%. That means the company has plenty of room to pay the distribution.

The distribution history is short. As a combined company, it has paid a distribution for only six quarters. Each time, it paid investors $0.31 per unit (partnerships have units, not shares).

So the track record is short, but there are no distribution cuts to penalize the stock’s dividend safety rating.

The only downside is its debt. The company’s net debt is nearly five times its earnings before interest, taxes, depreciation and amortization (EBITDA). That’s too high, and it puts a dent in the rating.

That being said, investors don’t have to worry too much. The company’s cash flow more than covers its interest expense. As long as cash flow stays at current levels or continues to grow, and debt doesn’t increase, the debt shouldn’t be a problem.

But it’s something to keep an eye on.

Other than that one issue, investors should continue to enjoy their 9.7% yield for years to come.

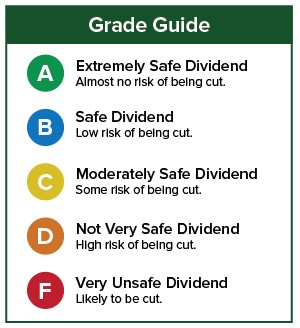

Dividend Safety Rating: B

If you have a stock whose dividend safety you’d like me to analyze, leave the ticker in the comments section.

[adzerk-get-ad zone="245143" size="4"]About Marc Lichtenfeld

Marc Lichtenfeld is the Chief Income Strategist of Investment U’s publisher, The Oxford Club. He has more than three decades of experience in the market and a dedicated following of more than 500,000 investors.

After getting his start on the trading desk at Carlin Equities, he moved over to Avalon Research Group as a senior analyst. Over the years, Marc’s commentary has appeared in The Wall Street Journal, Barron’s and U.S. News & World Report, among other outlets. Prior to joining The Oxford Club, he was a senior columnist at Jim Cramer’s TheStreet. Today, he is a sought-after media guest who has appeared on CNBC, Fox Business and Yahoo Finance.

Marc shares his financial advice via The Oxford Club’s free daily e-letter called Wealthy Retirement and a monthly, income-focused newsletter called The Oxford Income Letter. He also runs four subscription-based trading services: Technical Pattern Profits, Lightning Trend Trader, Oxford Bond Advantage and Predictive Profits.

His first book, Get Rich with Dividends: A Proven System for Earning Double-Digit Returns, achieved bestseller status shortly after its release in 2012, and the second edition was named the 2018 Book of the Year by the Institute for Financial Literacy. It has been published in four languages. In early 2018, Marc released his second book, You Don’t Have to Drive an Uber in Retirement: How to Maintain Your Lifestyle without Getting a Job or Cutting Corners, which hit No. 1 on Amazon’s bestseller list. It was named the 2019 Book of the Year by the Institute for Financial Literacy.