- Financial analysts crunch a seemingly infinite amount of data in an attempt to divine the future of the market.

- But as Nicholas Vardy explains today, their long-term predictions often miss the mark.

“Prediction is hard, especially about the future.”

– Yogi Berra

The Greeks turned to the Oracle of Delphi. The Romans interpreted animal entrails. Today, Wall Street analysts crunch endless data to divine the future.

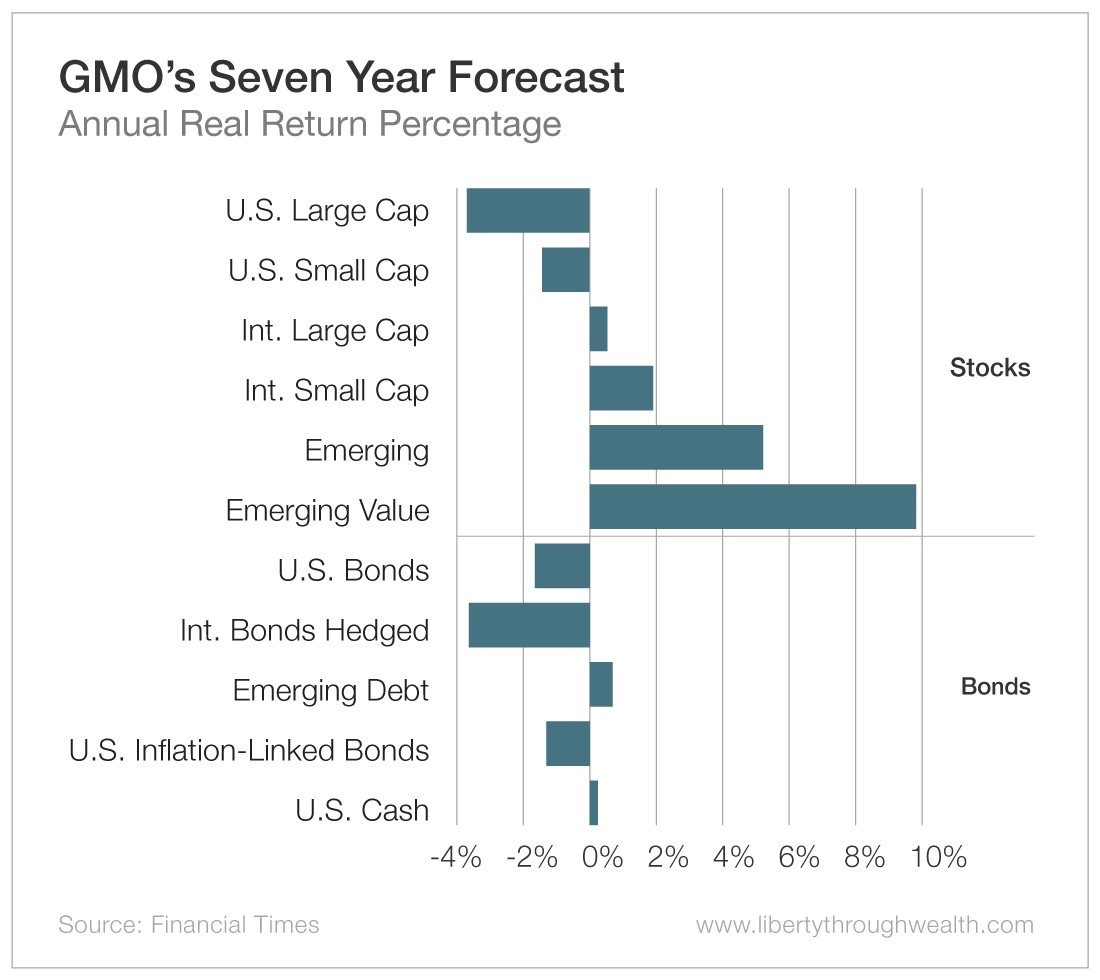

In today’s tradition, Boston money management firm GMO just published its annual outlook for all major asset classes for the seven years ahead.

Two predictions stood out.

First, GMO expects emerging market stocks to rise an average of 5.2% per year over the next seven years. Invest in the cheapest companies in emerging markets, and that expected return jumps to 9.8%.

Second, GMO predicts a negative 3.7% return per year for U.S. large cap stocks between now and 2026.

Both of these predictions may leave you scratching your head.

After all, if you’ve made money in U.S. stocks over the last decade and you’ve only lost money in emerging markets, you probably expect this set to continue.

The trend may shift in favor of emerging markets, as GMO predicts. Or it may not.

The truth is, your guess is at least as good as GMO’s.

Let me explain…

Lousy Predictions, Lousy Returns

Here’s why you should take GMO’s prediction – and any comparable ones – with a grain of salt.

GMO’s predictions are hardly manna from heaven.

Review GMO’s predictions since 2010, and you’ll find that they weren’t that different from what they are today.

And GMO’s 2010 predictions weren’t just off. They were way off…

Compare GMO’s seven-year predictions made in 2010 with how things turned out:

- GMO predicted no gains for U.S. large cap and U.S. small cap stocks from 2010 to 2017. In fact, the U.S. stock market just about doubled.

- International developed large cap and international small cap stocks fared much better than GMO had forecast.

- GMO expected emerging market stocks to fare the best, rising by about one-third. Instead, they stayed flat.

- Only bonds fared about as expected.

Excuses, Excuses (or We’re Too Smart to Be Wrong)

GMO would, of course, retort that its predictions weren’t wrong. They were just early.

And the fact that GMO has been wrong for almost 10 years makes the impending bounce in emerging markets all the more likely – and extreme.

Ditto for its prediction of the impending “Japanification” of the U.S. stock market – which implies decades of stagnation.

Here’s the harsh reality: GMO has been consistently wrong. And this has cost investors who followed its advice a lot of money.

GMO’s consistent errors highlight two recurring problems about predicting financial markets.

First, market analysts consistently overestimate their ability to predict the future.

I’m sure GMO has an able team of financial analysts who develop sophisticated models that crunch an ever-growing amount of data. But all that data just gives them a misplaced self-confidence.

Second, the mental model behind their predictions – reversion to the mean – is a lousy way to time the markets.

Yes, a market can be overvalued or undervalued for only so long. By analogy, a rubber band can stretch only so far before it snaps back.

So the current undervaluation of emerging market stocks portends massive outperformance in the future. The problem is that rubber bands can stretch a lot farther than we think.

All of this hints at a third problem – one that GMO and other analysts ignore…

GMO makes predictions about the future returns on an asset class, but it never calculates how much following its earlier advice cost investors.

Put another way, it doesn’t calculate the opportunity cost of holding underperforming assets.

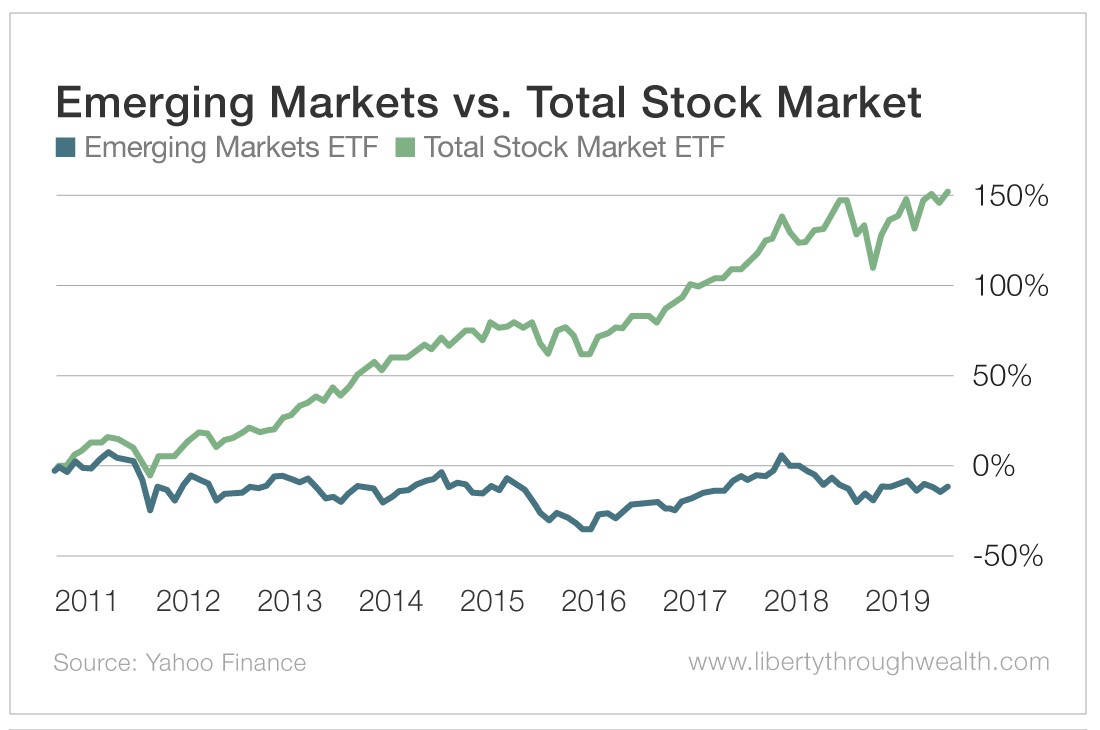

Say you took GMO’s advice and invested $10,000 on October 1, 2010, in the Vanguard FTSE Emerging Markets Index Fund ETF Shares (NYSE: VWO). By definition, you couldn’t invest that same amount in, say, U.S. stocks.

Fast-forward to today, and that $10,000 invested in the Emerging Markets ETF would be worth $8,899.

Had you taken that same $10,000 and invested it in the U.S. stock market as represented by the Vanguard Total Stock Market ETF (NYSE: VTI), your investment would have been worth $25,224.

That’s a big difference.

Say emerging market value stocks take off tomorrow.

How long will it take for them to catch up to the U.S. stock market? Even under the best of conditions, it will take half a decade at best.

And those are years that you may not have.

The bottom line? Ignore forward-looking stock return forecasts like GMO’s.

They will almost certainly be wrong. By a lot.

[adzerk-get-ad zone="245143" size="4"]About Nicholas Vardy

An accomplished investment advisor and widely recognized expert on quantitative investing, global investing and exchange-traded funds, Nicholas has been a regular commentator on CNN International and Fox Business Network. He has also been cited in The Wall Street Journal, Financial Times, Newsweek, Fox Business News, CBS, MarketWatch, Yahoo Finance and MSN Money Central. Nicholas holds a bachelor’s and a master’s from Stanford University and a J.D. from Harvard Law School. It’s no wonder his groundbreaking content is published regularly in the free daily e-letter Liberty Through Wealth.