PacWest Bancorp (Nasdaq: PACW) is a small California bank with 76 branches.

The stock pays a $0.60 per share quarterly dividend, which comes out to a whopping 6.4% yield. That’s strong for a bank that isn’t considered particularly speculative.

This is an interesting situation because at face value, the dividend looks perilous.

The company cut the dividend in 2009 and 2010. SafetyNet Pro penalizes stocks with dividend cuts in the past 10 years.

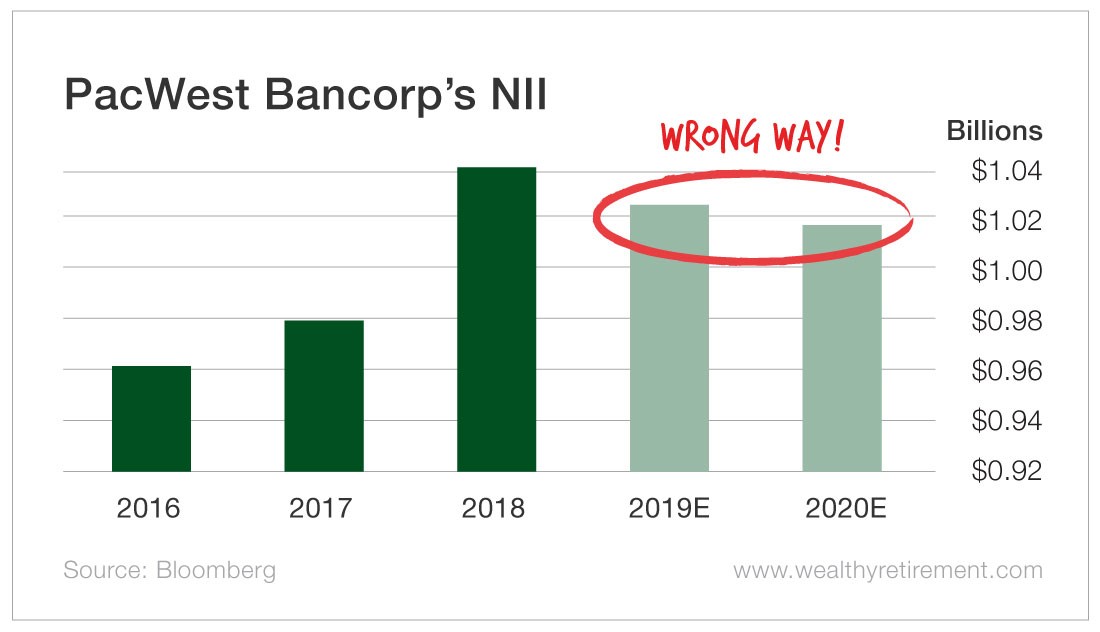

Net interest income (NII), the measure that we use to analyze a bank’s ability to pay a dividend, rose for the past few years, but this year and next year NII is forecast to dip.

We don’t like to see cash flow or NII going the wrong way on dividend-paying companies.

Here’s the thing: While NII is expected to head lower, this year the forecast is a decline of 1.5%. Next year, it’s expected to slip less than 1%.

That is a tiny margin of error. Should NII growth be positive instead of negative, the stock will receive an upgrade from SafetyNet Pro.

And if growth is expected in 2021, it would be a significant upgrade.

The positive news is that the payout ratio is very low. So even though NII is projected to decline, PacWest Bancorp pays out less than 30% of its NII in dividends.

That low payout ratio gives me confidence that the dividend will not be reduced, despite the stock’s low rating due to falling NII and two dividend cuts.

And those dividend cuts are about to age out. Remember, SafetyNet Pro dings a company for lowering its dividend in the past 10 years. The 2009 cut will age out on January 1.

So all else being equal, the stock should see an upgrade early next year. Once 2010’s cut is older than 10 years, that will mean another upgrade.

So it’s possible that if NII shows positive growth this year and estimates climb for 2021, we could see PacWest Bancorp elevated all the way to an “A” rating for dividend safety.

This is an interesting situation because NII is headed south, which we don’t want to see, yet the payout ratio is low and the company will soon have a solid, 10-year dividend-raising track record.

Right now, because of the two dividend cuts in its recent history and lower forecast NII, the rating is low. But an upgrade should be coming very soon – possibly a big upgrade.

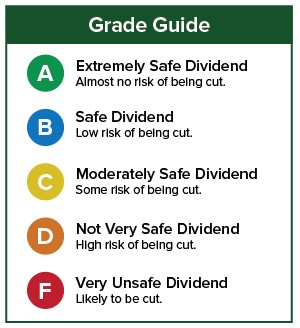

Dividend Safety Rating: D

Have a great Thanksgiving.

If you have a stock whose dividend safety you’d like me to analyze, leave the ticker symbol in the comments section.

[adzerk-get-ad zone="245143" size="4"]About Marc Lichtenfeld

Marc Lichtenfeld is the Chief Income Strategist of Investment U’s publisher, The Oxford Club. He has more than three decades of experience in the market and a dedicated following of more than 500,000 investors.

After getting his start on the trading desk at Carlin Equities, he moved over to Avalon Research Group as a senior analyst. Over the years, Marc’s commentary has appeared in The Wall Street Journal, Barron’s and U.S. News & World Report, among other outlets. Prior to joining The Oxford Club, he was a senior columnist at Jim Cramer’s TheStreet. Today, he is a sought-after media guest who has appeared on CNBC, Fox Business and Yahoo Finance.

Marc shares his financial advice via The Oxford Club’s free daily e-letter called Wealthy Retirement and a monthly, income-focused newsletter called The Oxford Income Letter. He also runs four subscription-based trading services: Technical Pattern Profits, Lightning Trend Trader, Oxford Bond Advantage and Predictive Profits.

His first book, Get Rich with Dividends: A Proven System for Earning Double-Digit Returns, achieved bestseller status shortly after its release in 2012, and the second edition was named the 2018 Book of the Year by the Institute for Financial Literacy. It has been published in four languages. In early 2018, Marc released his second book, You Don’t Have to Drive an Uber in Retirement: How to Maintain Your Lifestyle without Getting a Job or Cutting Corners, which hit No. 1 on Amazon’s bestseller list. It was named the 2019 Book of the Year by the Institute for Financial Literacy.