A year ago, my colleague Kristin Orman looked at Tanger Factory Outlet Centers (NYSE: SKT) and determined the stock deserved a “B” rating for dividend safety. At the time, Kristin wrote…

We usually don’t like to see declining cash flows. But Tanger’s low payout ratio and history of raises make the dividend a safe bet.

However, if AFFO declines again in 2019, Tanger’s safety rating could fall with it.

AFFO stands for adjusted funds from operations – a measure of cash flow for real estate investment trusts (REITs).

The issue that caught Kristin’s eye was that at that point in 2018, management’s guidance for AFFO was lower than it had been the year before.

Let’s see if we still have reason for concern…

Tanger Factory Outlets owns and operates 39 outlet shopping centers in 20 states and Canada.

You may have seen recent news that vacancies at shopping malls hit an eight-year high in the third quarter. Nearly 10% of storefronts are vacant.

Tanger is holding up better than most. In the second quarter, it reported a 96% occupancy rate, which is up from 95.4% the previous quarter and 95.6% a year ago. However, it is down from 97% at the end of 2016.

In 2018, AFFO was better than management expected but still slightly below the 2017 total. This year, AFFO is forecast to shrink again, this time by a meaningful amount.

Now, recall that last year, management guided toward low AFFO and it came in higher than expected. So perhaps it’s sandbagging again this year so that the end results beat expectations.

But considering AFFO will likely be down for the second year in a row, it is something to keep an eye on.

Last year, the payout ratio was a comfortable 54%, though if this year’s results come in at the $164 million projected, the payout ratio will be 82%. This would be fine, but it would indicate that the payout was starting to get a little high.

Tanger does, however, have history on its side. It has raised its dividend for 25 years in a row.

The quarter-of-a-century track record of annual dividend raises is significant. Management has made it clear that the dividend is important.

I believe management will do whatever it can to continue to raise the dividend, which is currently yielding 9.8%. However, the lower cash flow is a concern.

I’ll keep an eye on it. But for the near future, the dividend appears safe.

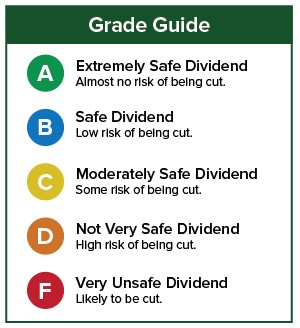

Dividend Safety Rating: B

If you have a stock whose dividend safety you’d like me to analyze, leave the ticker in the comments section.

You can also search the site to see if I’ve written about your favorite stock recently. Just click the magnifying glass and type in the name of the company (names get better search results than ticker symbols).

[adzerk-get-ad zone="245143" size="4"]About Marc Lichtenfeld

Marc Lichtenfeld is the Chief Income Strategist of Investment U’s publisher, The Oxford Club. He has more than three decades of experience in the market and a dedicated following of more than 500,000 investors.

After getting his start on the trading desk at Carlin Equities, he moved over to Avalon Research Group as a senior analyst. Over the years, Marc’s commentary has appeared in The Wall Street Journal, Barron’s and U.S. News & World Report, among other outlets. Prior to joining The Oxford Club, he was a senior columnist at Jim Cramer’s TheStreet. Today, he is a sought-after media guest who has appeared on CNBC, Fox Business and Yahoo Finance.

Marc shares his financial advice via The Oxford Club’s free daily e-letter called Wealthy Retirement and a monthly, income-focused newsletter called The Oxford Income Letter. He also runs four subscription-based trading services: Technical Pattern Profits, Lightning Trend Trader, Oxford Bond Advantage and Predictive Profits.

His first book, Get Rich with Dividends: A Proven System for Earning Double-Digit Returns, achieved bestseller status shortly after its release in 2012, and the second edition was named the 2018 Book of the Year by the Institute for Financial Literacy. It has been published in four languages. In early 2018, Marc released his second book, You Don’t Have to Drive an Uber in Retirement: How to Maintain Your Lifestyle without Getting a Job or Cutting Corners, which hit No. 1 on Amazon’s bestseller list. It was named the 2019 Book of the Year by the Institute for Financial Literacy.