- The Yale endowment model has enjoyed massive success and inspired many copycats, but over the last decade, it has lagged the market.

- Today, Nicholas Vardy explains why and what investors can learn from this investment strategy.

David Swensen, manager of the Yale endowment and the university’s chief investment officer, is smarting.

Yale recently announced that its endowment returned a paltry 5.7% over the past year. Yale’s results trailed those of its largest rivals, Harvard and Stanford – both of which returned 6.5%.

Not exactly eye-popping returns.

With the average billion-dollar-plus college endowment returning just 5.8%… It’s no wonder Bloomberg called this year’s crop of college endowment returns “ho-hum.”

Yale’s returns were particularly embarrassing… And its lagging returns have raised questions about an investment strategy that’s been sputtering for more than a decade.

Let me explain…

The Yale Model

Harvard may have a bigger endowment. But make no mistake… Yale has always been the big kahuna among top university endowments.

If imitation is the sincerest form of flattery, the Yale endowment has been flattered like no other. Most of Yale’s academic rivals have spent the last two decades adopting the “Yale model” of investing.

The endowments at Stanford, Princeton, MIT and University of Pennsylvania are each headed by former protégés of Swensen. Each is hoping some of Yale’s magic will rub off on its funds.

Yale’s Secret Sauce

Swensen was the first to apply the modern portfolio theory (MPT) taught in finance textbooks to multibillion-dollar university endowments.

MPT teaches that if you diversify across asset classes beyond U.S. stocks and bonds, you can generate higher returns at a lower risk. (This is also the fundamental insight behind The Oxford Communiqué‘s Gone Fishin’ Portfolio.)

Swensen took diversification to its logical extreme.

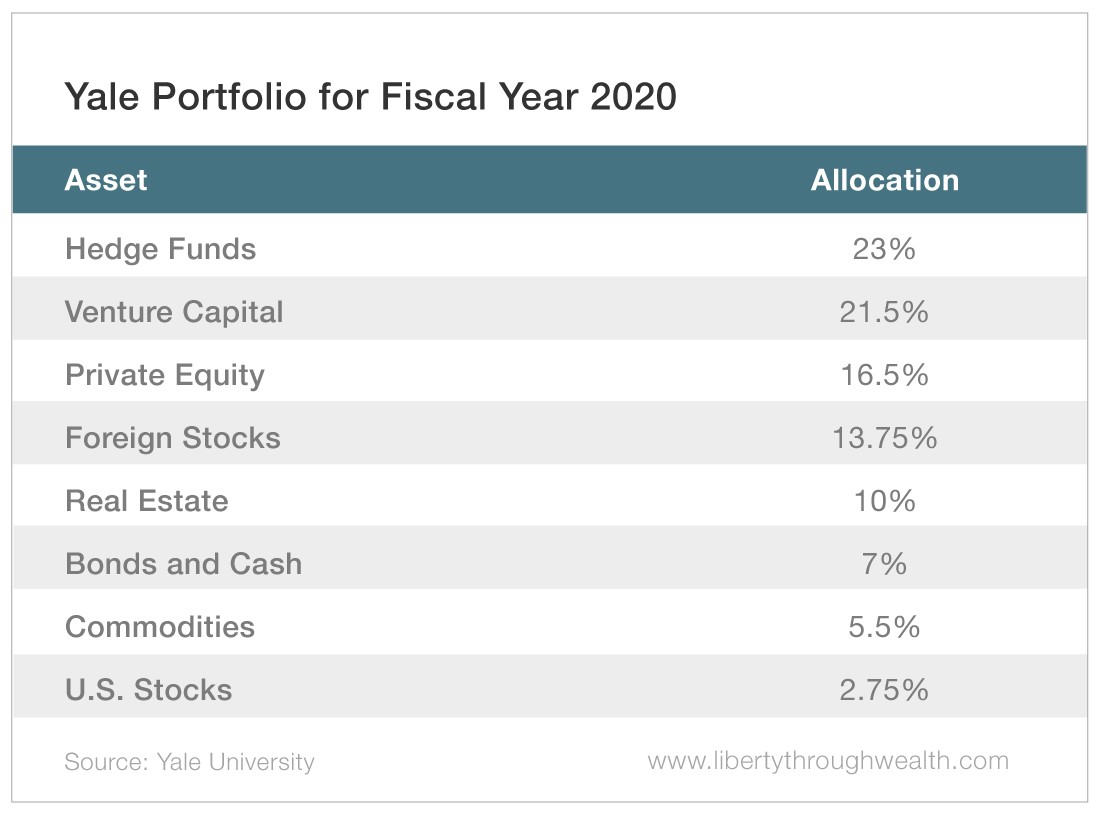

Over the past 30 years, Yale shifted the bulk of its investments into “alternative assets.” These assets include natural resources, venture capital, real estate and foreign stocks.

The result? The Yale endowment looks very different from your investment portfolio.

It’s always hard to argue with success. And until June 2007, it was impossible to argue with Yale.

In the 10 years prior to 2007, the Yale endowment returned a remarkable 17.8% per year.

The global financial crisis of 2008 changed all that. Over the past decade, Yale’s returns dropped to just 11.1% per year – substantially trailing the S&P 500’s 14.7% return over the same period.

Swensen’s Big Bet Goes Awry

One big bet stands out in Yale’s portfolio: its tiny allocation to U.S. stocks.

As it turns out, Yale has been underweight U.S. stocks for decades.

Its weighting in U.S. stocks tumbled from 80% in 1987 to 22% in 1995. By 2005, it had dropped to 14%. For 2020, U.S. stocks make up a trivial 2.75% of its portfolio.

Put another way, a whopping 97.25% of Yale’s endowment is invested in assets other than U.S. stocks!

Here’s where Swensen went awry…

Because the U.S. stock market has been the top-performing major stock market in the world over the past decade, Swensen’s bet against U.S. stocks has cost Yale dearly.

With Yale’s annual return of 11.1% lagging the S&P 500’s 14.7% return by 3.1% a year over 10 years, the value of forgone profits on Yale’s endowment easily goes into the billions of dollars.

Has Yale’s Secret Sauce Turned Sour?

Underweighting U.S. stocks – and betting big on commodities, international stocks and emerging markets – has cost Yale billions in potential profits.

At the same time, Yale’s even bigger bets on private equity and venture capital have paid off handsomely.

So the Yale endowment didn’t lag the U.S. stock market because diversification is dead. It lagged the U.S. stock market because the past decade’s strength is a historical anomaly.

U.S. stocks will keep trouncing other asset classes. Until one day, they won’t.

Once the tide turns – as it inevitably will – Yale will again end up on top.

[adzerk-get-ad zone="245143" size="4"]About Nicholas Vardy

An accomplished investment advisor and widely recognized expert on quantitative investing, global investing and exchange-traded funds, Nicholas has been a regular commentator on CNN International and Fox Business Network. He has also been cited in The Wall Street Journal, Financial Times, Newsweek, Fox Business News, CBS, MarketWatch, Yahoo Finance and MSN Money Central. Nicholas holds a bachelor’s and a master’s from Stanford University and a J.D. from Harvard Law School. It’s no wonder his groundbreaking content is published regularly in the free daily e-letter Liberty Through Wealth.